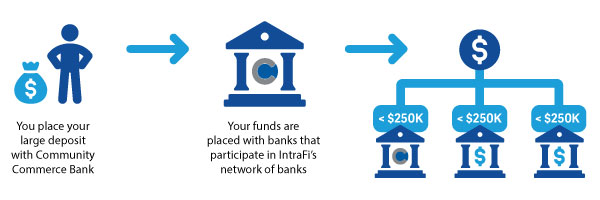

A Smart, Convenient Way to Protect

Large Deposits.

Our Branches and Customer Service will be closing at 12pm PDT on Friday, April 3rd for Good Friday.

Our Branches and Customer Service will be closed Tuesday, March 31st in observance of Cesar Chavez Day.

Our Branches and Customer Service will be closed Monday, May 25th for Memorial Day.

Our Branches and Customer Service will be closed Friday, June 19th for Juneteenth.

Our Branches and Customer Service will be closed Friday, July 3rd in Observance of Independence Day.

Our Branches and Customer Service will be closed Monday, September 7th for Labor Day.

Our Branches and Customer Service will be closed Monday, October 12th for Columbus Day.

Our Branches and Customer Service will be closed on Wednesday, November 11th in honor of Veterans Day.

Our Branches and Customer Service will be closed Thursday, November 26th & Friday, November 27th for Thanksgiving.

Our Branches and Customer Service will close at 12pm PST on Thursday, Dec 24th and all day Friday, Dec 25th for Christmas.

Our Branches and Customer Service will close at 12pm PST on Tuesday, Dec 31st and all day Wednesday, Jan 1st for New Years.

Our Branches and Customer Service will be closed on Monday, January 19th in observance of Martin Luther King Jr. Day.

Our Branches and Customer Service will be closed Monday, February 16th for Presidents' Day.

Our Branches and Customer Service will close at 12pm PST on Thursday, Dec 31st and all day Friday, Jan 1st for New Years.